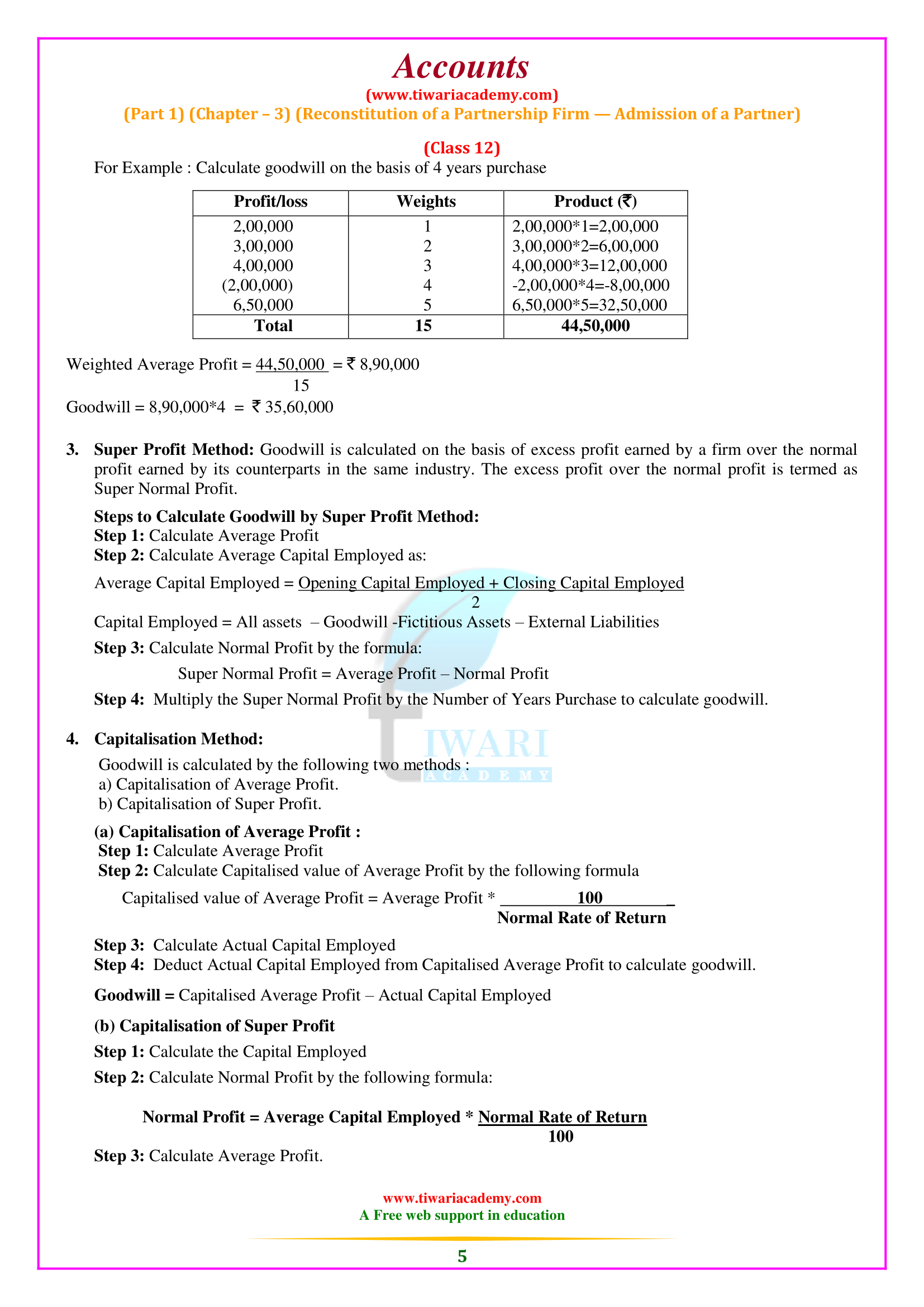

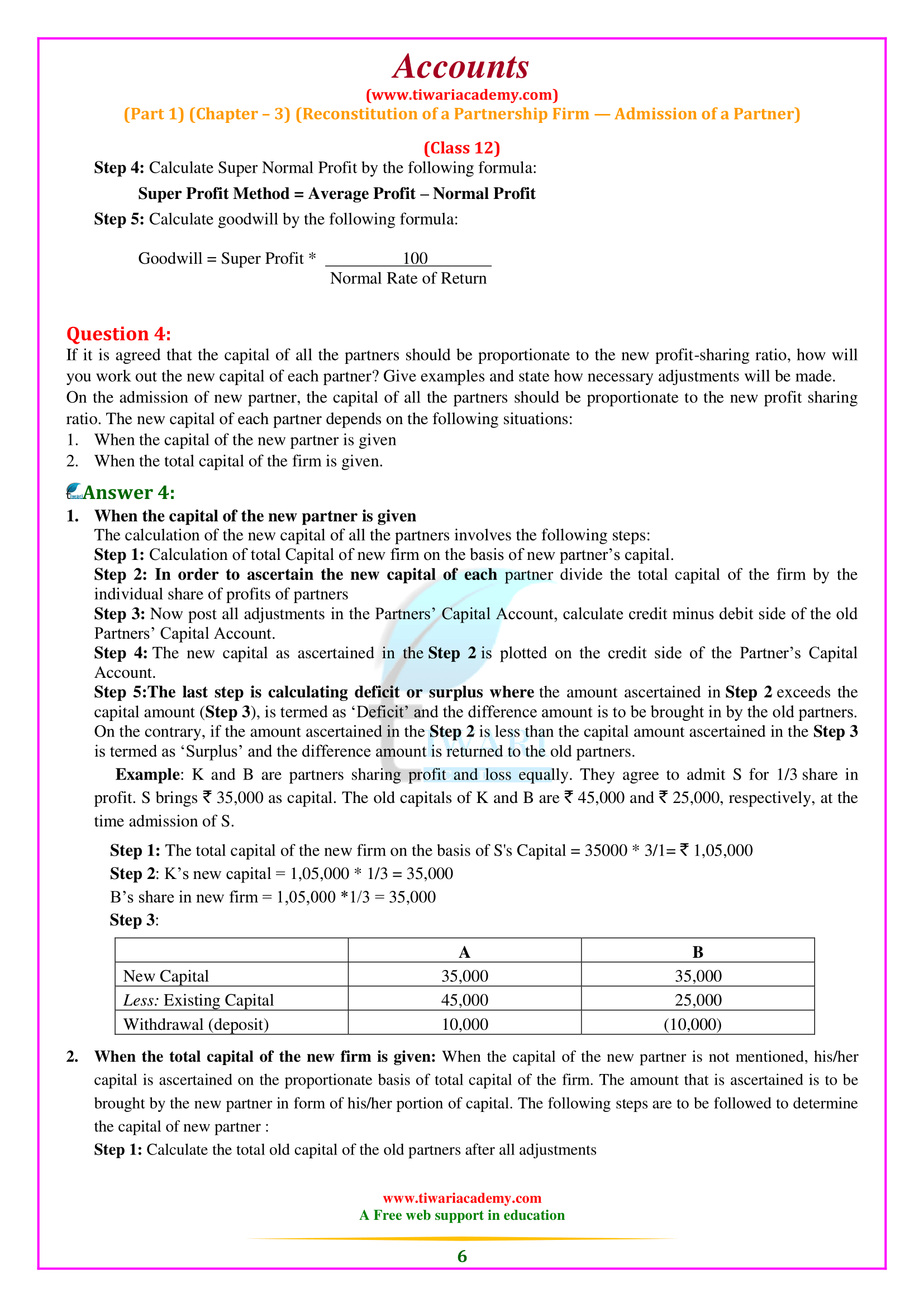

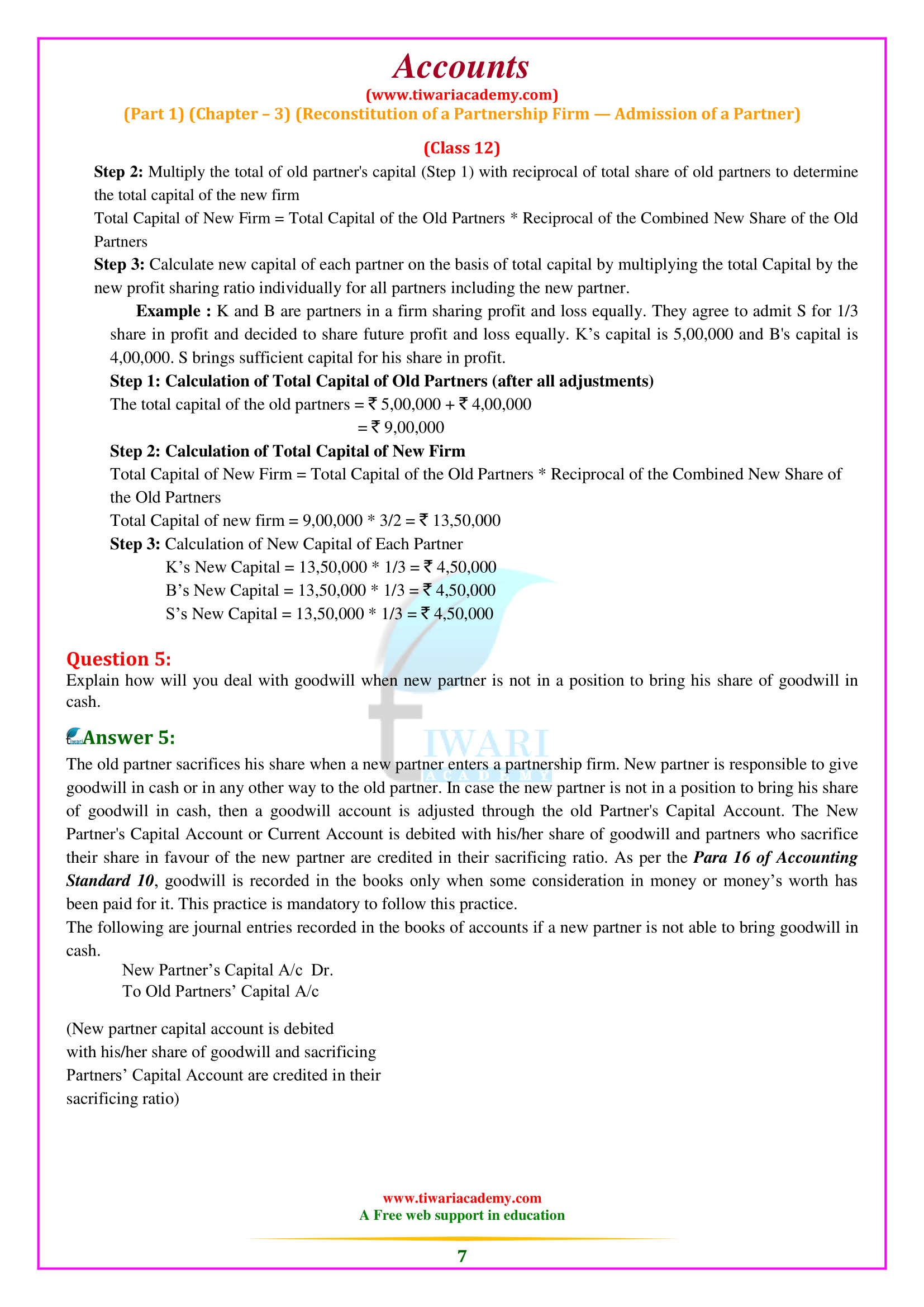

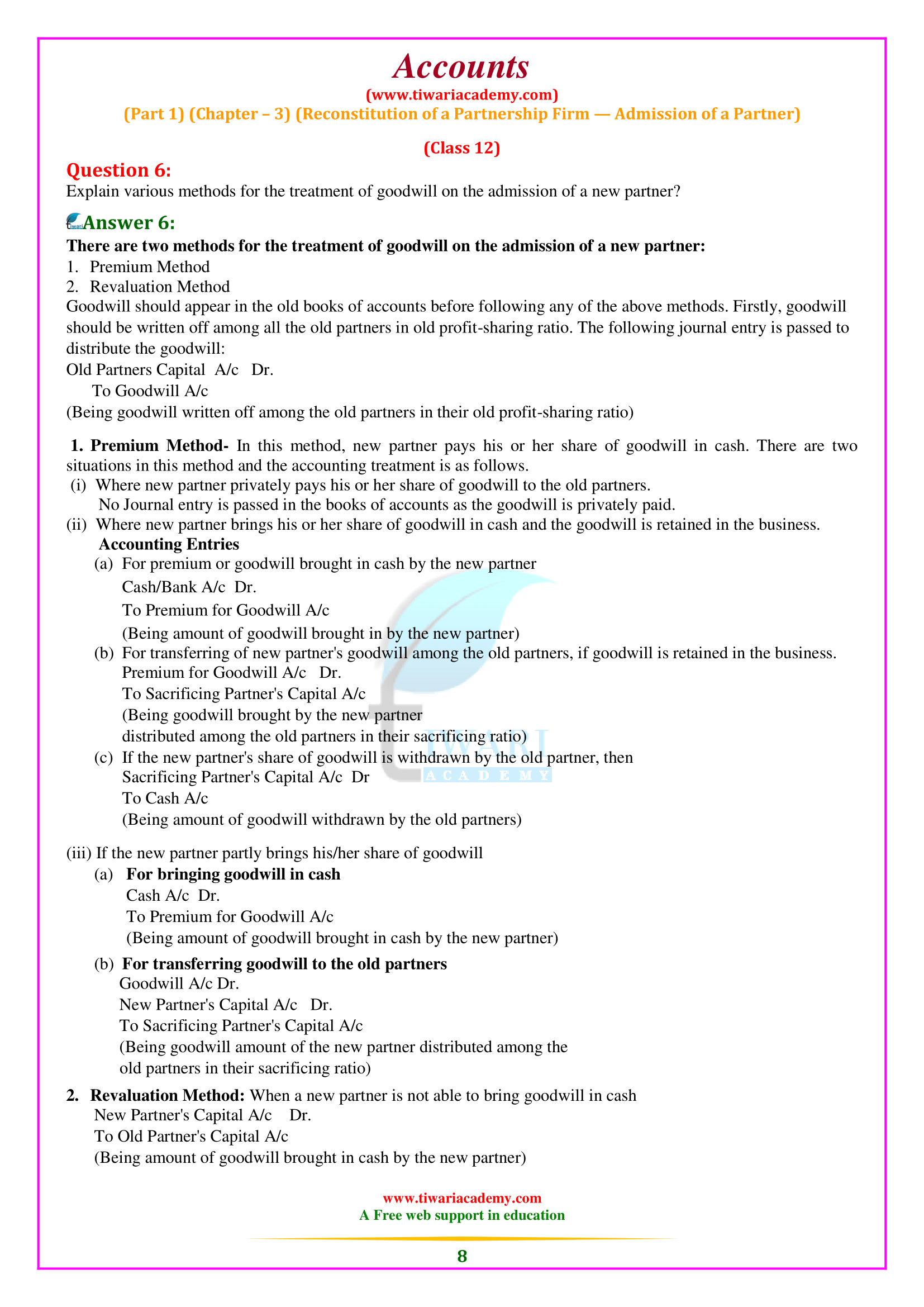

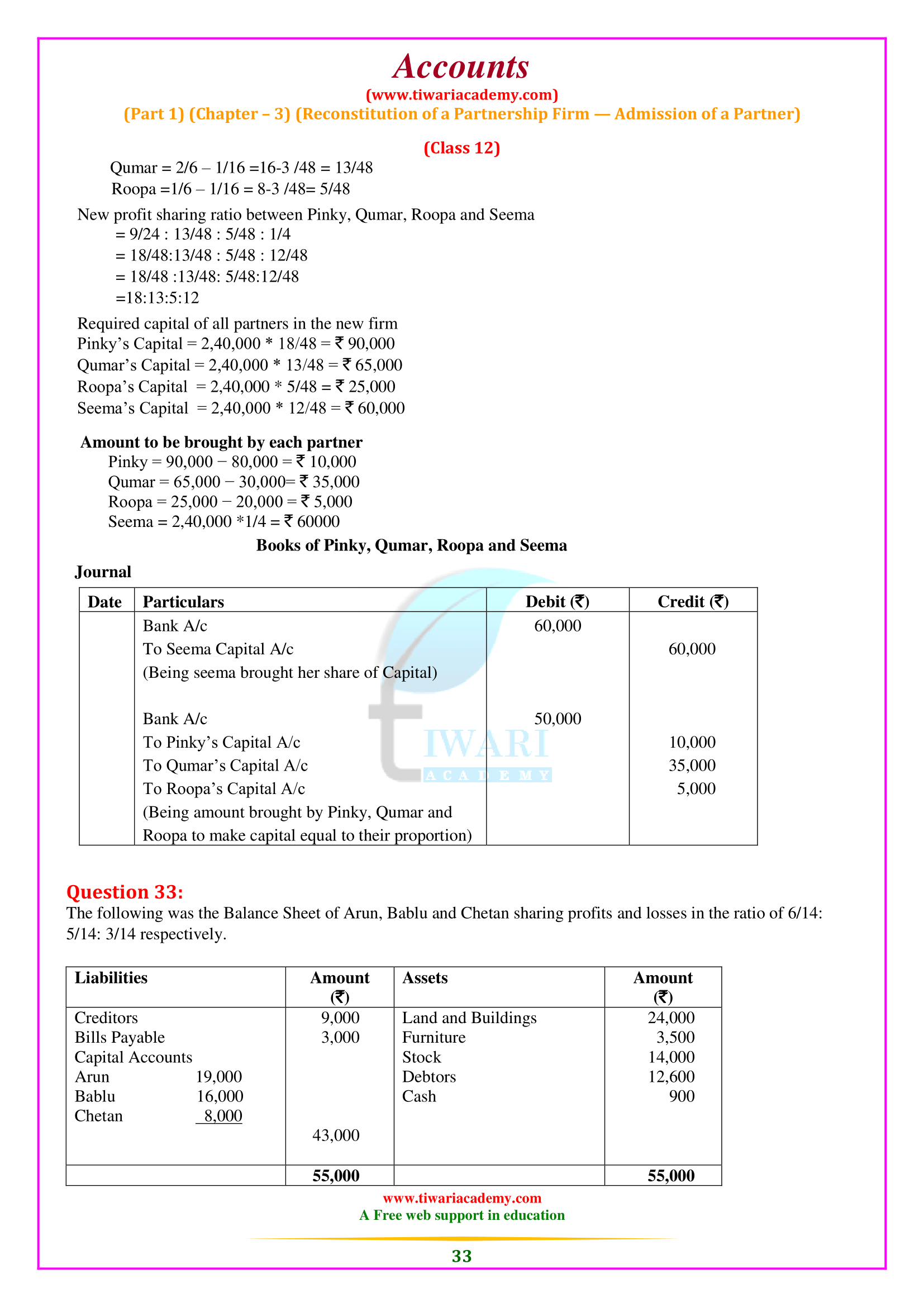

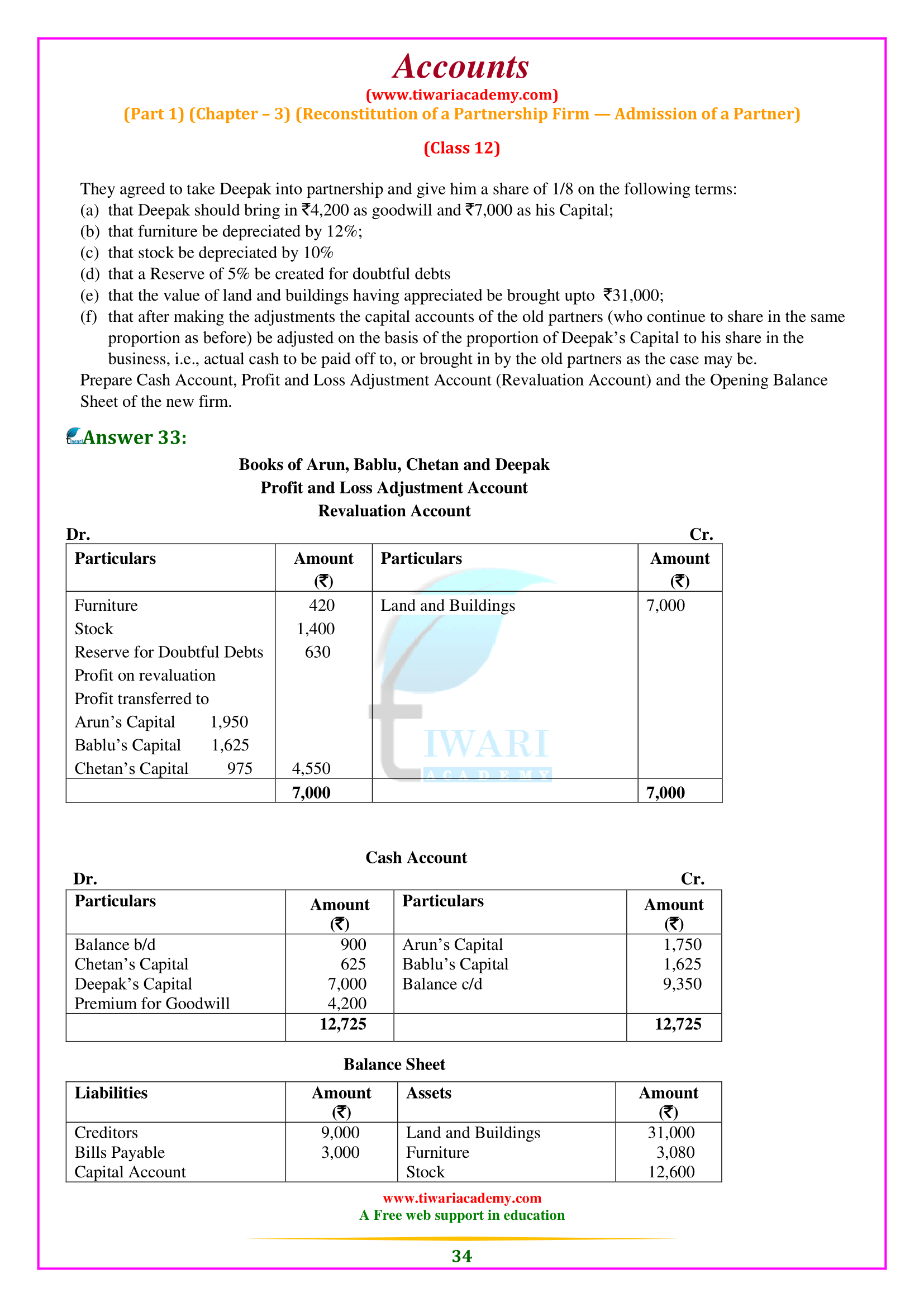

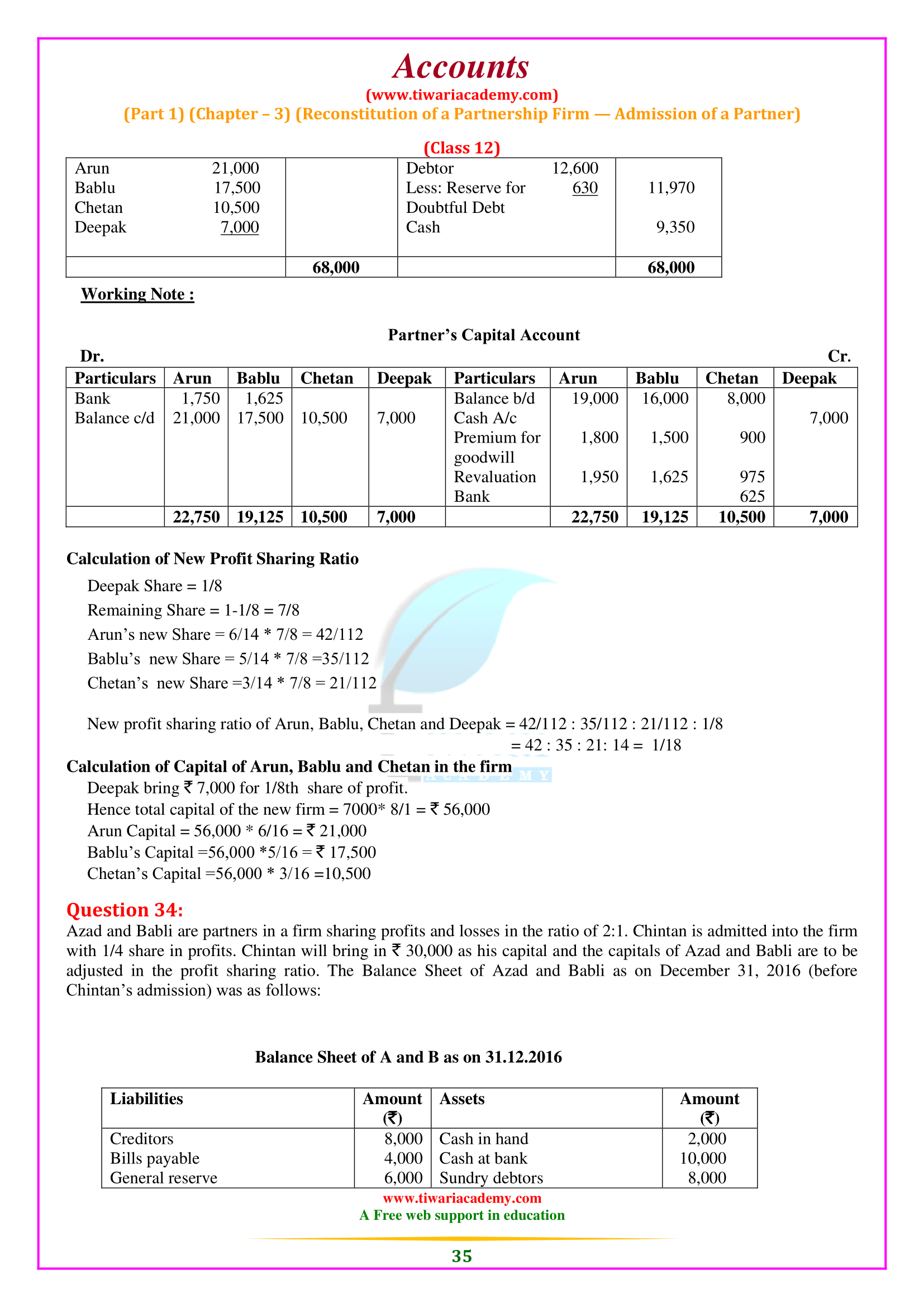

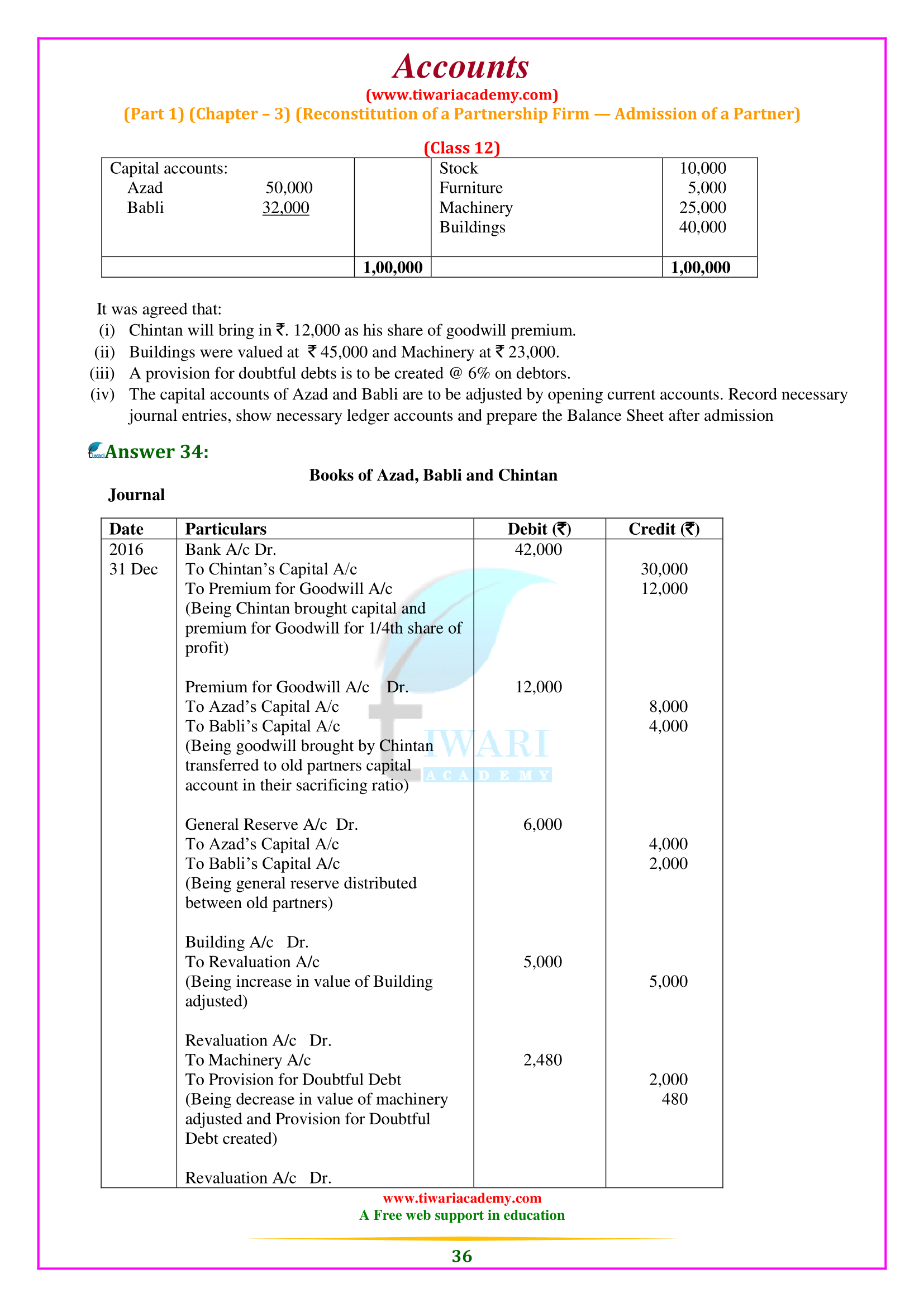

by Tiwari Academy

NCERT Solutions for Class 12 Accountancy Chapter 3 Part 1 Reconstitution of a Partnership Firm-Admission of a Partner. Students can get here the suitable answers of NCERT Textbook’s questions and notes related to chapter 3 of plus two accounts. All the questions are described properly in simple language with examples, so that students can understand easily. Extra questions and notes are available in the format of PDF file to free download.

Class 12 Accountancy Chapter 3 Question Answers

NCERT Solutions for Class 12 Accountancy Chapter 3 Admission of a Partner

| Class: 12 | Accountany (Part 1) |

| Chapter: 3 | Reconstitution of a Partnership Firm-Admission of a Partner |

| Contents: | NCERT Solutions and Notes |

Modes of Reconstitution of a Partnership Firm

Admission of a new partner

A new partner may be recruited if additional capital or administrative help is required. According to the provisions of the Companies Act of 1932, unless otherwise provided in the partnership deed, a new partner can only be accepted if the existing partners agree unanimously. For example, Hari and Tiwari are 3: 2 profit-sharing partners. On April 1, 2017, John was recruited as a new partner with 1/6 share of its profits. With this change, the firm now has three partners and has been reorganized.

Download NCERT Solution App

Changes in profit sharing ratio between existing partners

Sometimes, partners in a company may decide to change their current profit sharing ratio. This may result from a change in the role of existing partners in the company. For example, Ram, Mohan, and Sohan are partners in a company that shares profits in a 3: 2: 1 ratio. As of April 1, 2017, they decided to share the profits equally, as Sohan brings additional capital. This changes the existing agreement leading to the restructuring of the company.

Return of current partner

This means withdrawal by a partner from the firm’s business, which may be due to poor health, old age, or a change in business interests. The partner can withdraw at any time if the partnership is at will. For example, Roy, Ravi, and Rao are partners in the company, who share profits in the ratio 2: 2: 1. Due to illness, Ravi withdrew from the firm on March 31, 2017. This resulted in the reorganization of the company. The firm now has only two partners.

Partner’s death

The partnership can be restructured even after the partner’s death if the remaining partners decide to continue the company’s business as usual. For example, X, Y, and Z are partners in a company that shares profits in 3: 2: 1. X died on March 31, 2017. Y and Z decide to continue the business, sharing future profits equally. The company is restructured by continuing the business of equally distributing Y and Z’s future profits.

Factors Affecting the Value of Goodwill

The main factors affecting the value of goodwill are as follows:

- Nature of business: A company that produces high value-added products or a stable demand can earn more profit and therefore has more goodwill.

- Location: If the business is centrally located or high customer traffic, goodwill becomes high.

- Management efficiency: A well-managed company often takes advantage of high productivity and profitability. This leads to higher profits, and hence the value of goodwill will also be higher.

- Market conditions: A monopoly or limited competition situation allows a company to achieve higher profits, thus higher the value of goodwill.

- Notable benefits: Firms that receive unique benefits such as import licenses, low tariffs, and assured power supplies, long term material supply contracts, recognized affiliates, patents, trademarks, etc. The value of goodwill is high.

What are the point that must be considered at the time of admission of a new partner 12th Accounts Chapter 3?

Main points which require attention at the time of admission of a new partner:

1. New profit sharing ratio.

2. Sacrificing ratio.

3. Valuation and adjustment of goodwill.

4. Revaluation of assets and Reassessment of liabilities.

5. Distribution of accumulated profits.

6. Adjustment of partners’ capitals.

What is Goodwill in Class 12 Accounts Chapter 3?

Over a while, a well-established business develops the benefit of a good name, reputation, and broad business connections. This helps the company to earn more profit than the newly created company. In accounting, the monetary value of that profit is known as “goodwill.”

What are the rights of a newly admitted partner in 12th Accountancy Chapter 3?

A newly admitted partner acquires two main rights in the firm:

1. Right to share the assets of the partnership firm.

2. Right to share the profits of the partnership firm.

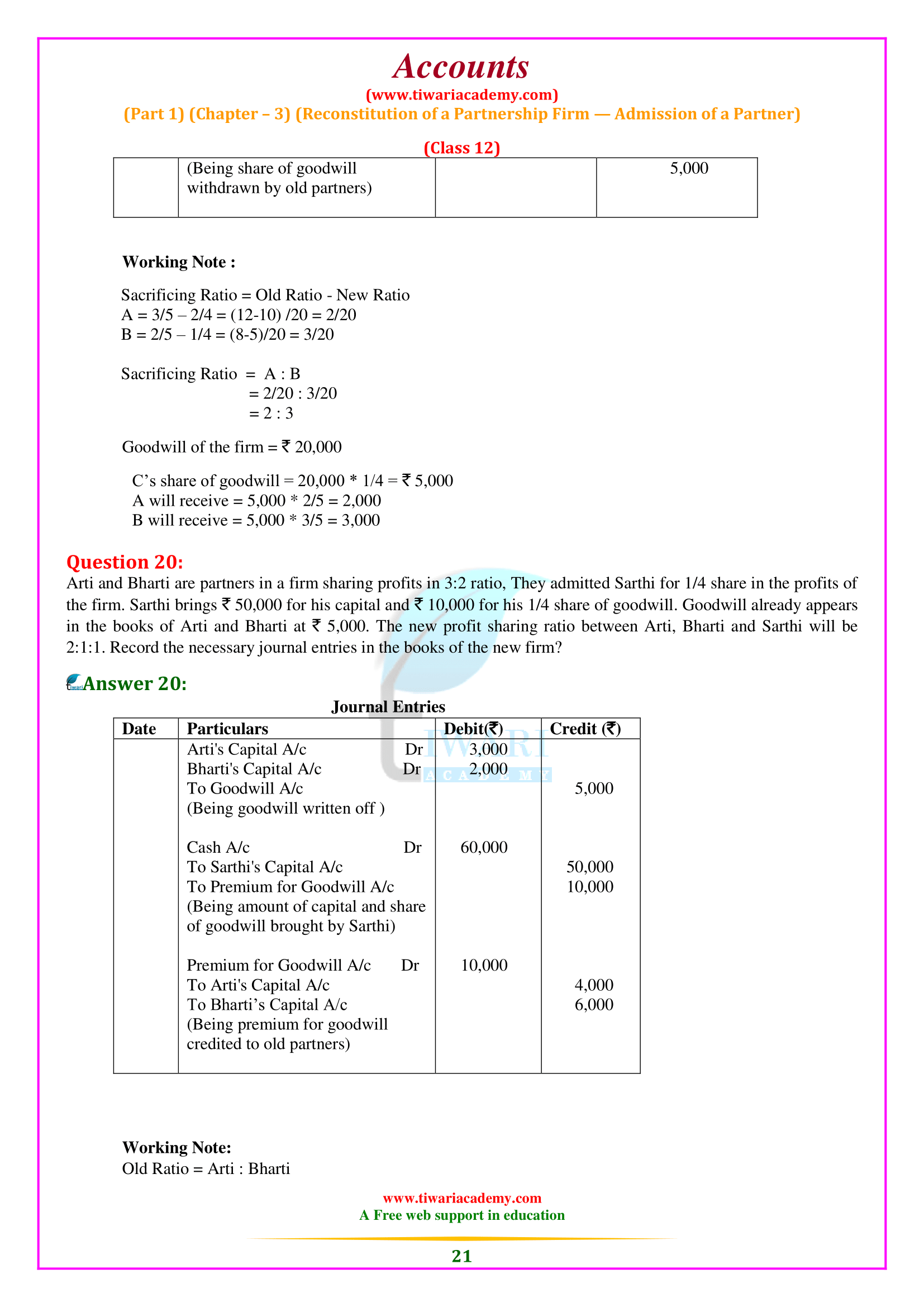

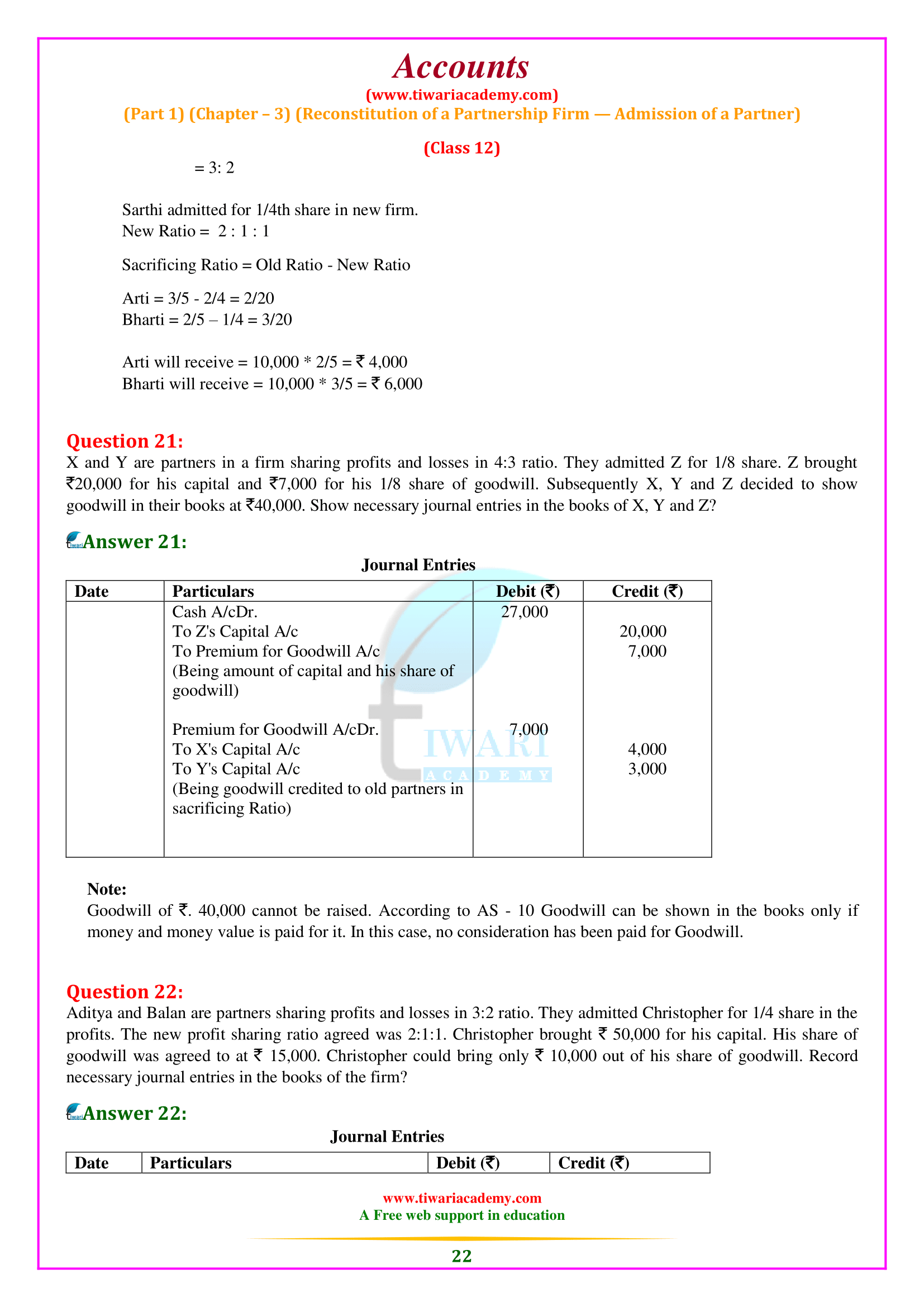

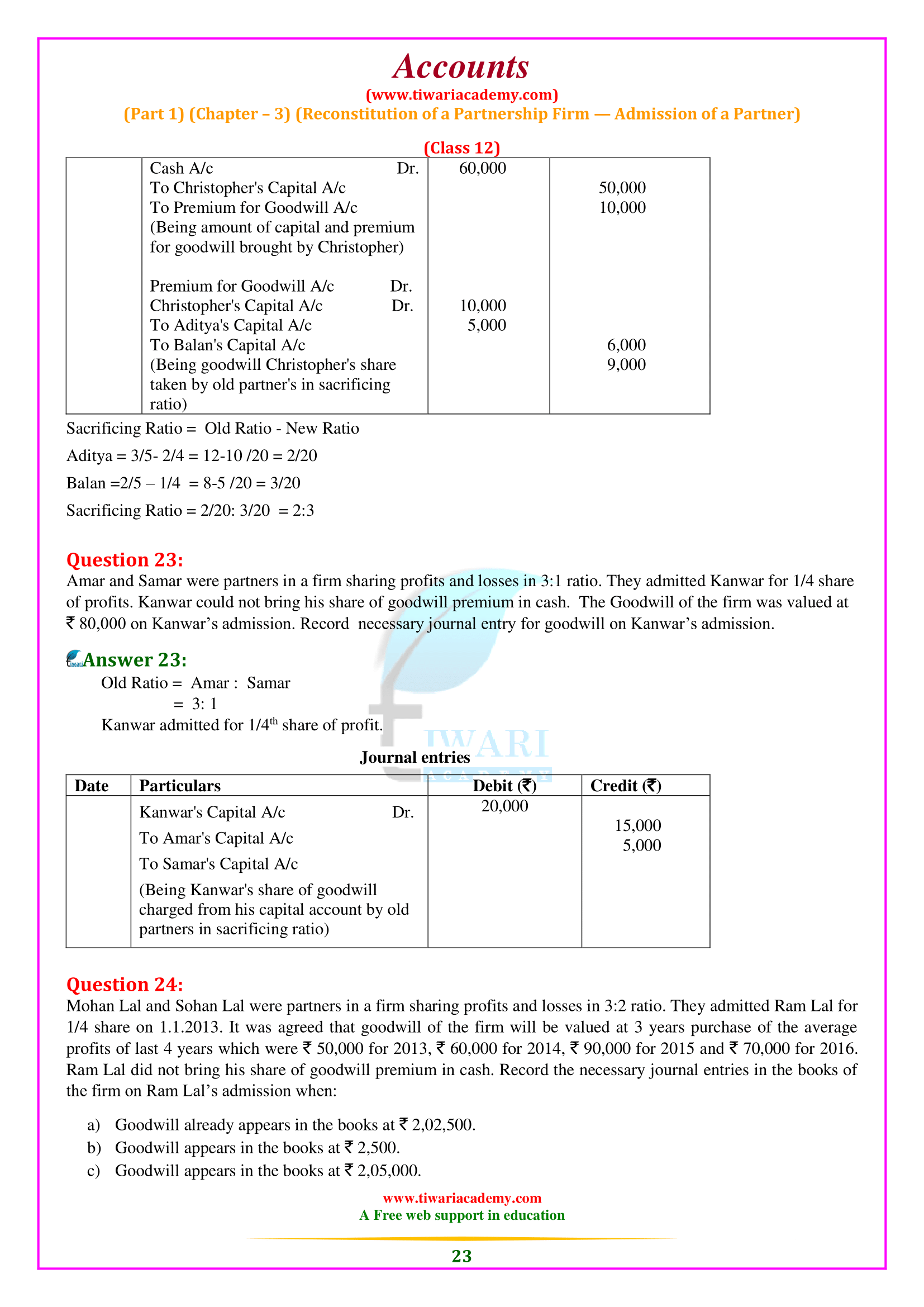

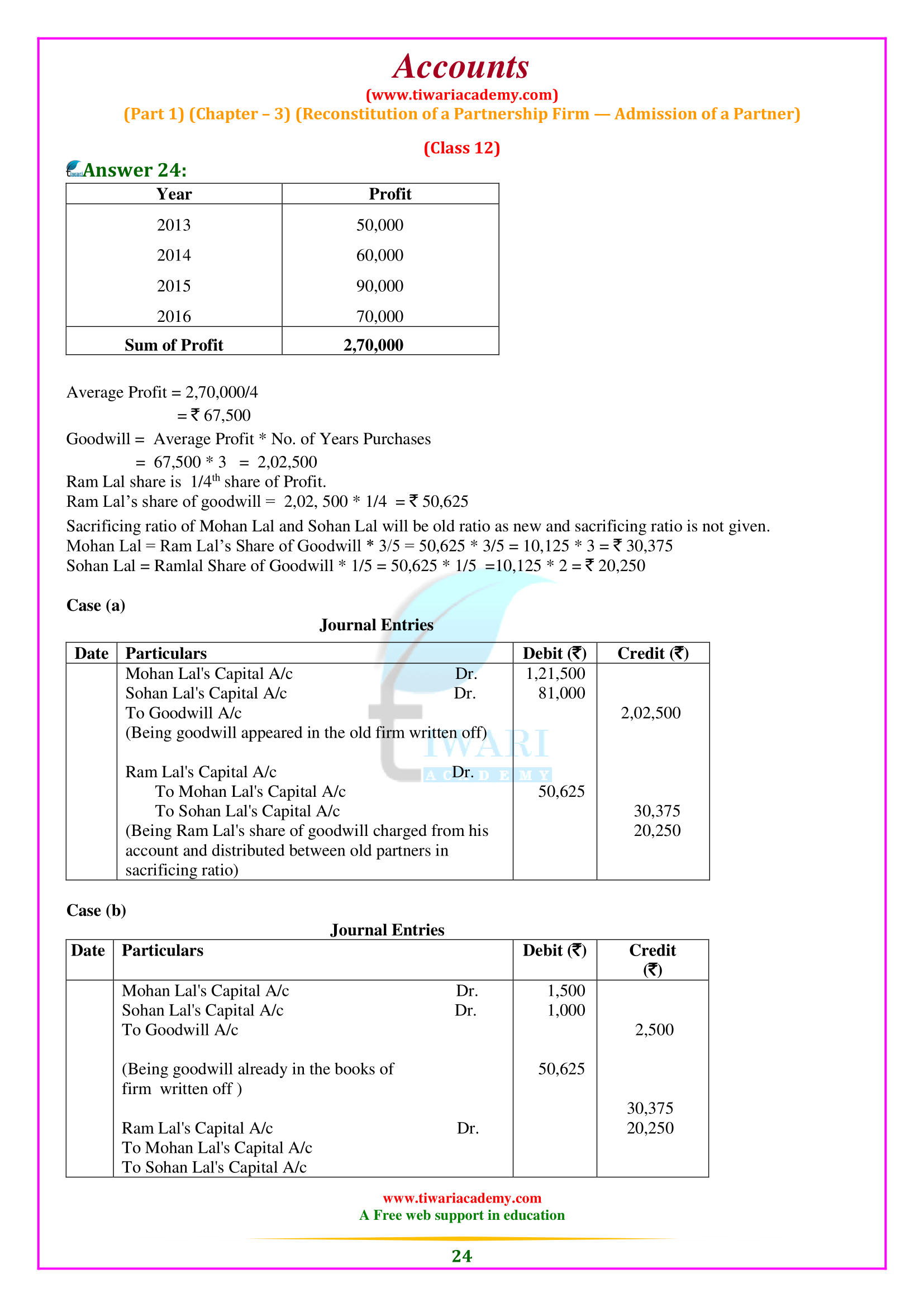

This amount is shared by the existing partners in the ratio in which they forgo their shares in favor of the new partner which is called sacrificing ratio.